{kind=link}

Read here: Spotlight on…financial resilience (PDF)

Millions of households in the UK lack the savings that would help them weather financial shocks. In 2024, just under one in ten adults (9%) would only be able to cover their living expenses for up to a week if they lost their main source of income, and almost two in five adults (38%) did not have enough in savings to cover a £250 emergency expense.[1] Among low- and moderate-income households, this number is even greater, with just over half of households (52%) saying they would not be able to cover a £250 expense from their savings.[2]

From an individual and an equity perspective, we know there are good reasons to support financial resilience. What we know less about is how these individual-level effects feed into the wider economy. How does our ability to weather financial shocks (or not) affect our health, our wellbeing, how we perform at work, and how we interact with our families and communities?

This is one of the aims of the programme of work on financial resilience that Nest Insight embarked on in 2025: to assess the impact of improving financial resilience among workers with low and moderate incomes on the wider economy. As part of this programme, we have worked with PBE to develop a logic model that maps out key channels through which improved financial resilience might affect individuals, households and businesses. The model is designed to help us understand the wider economic impacts.

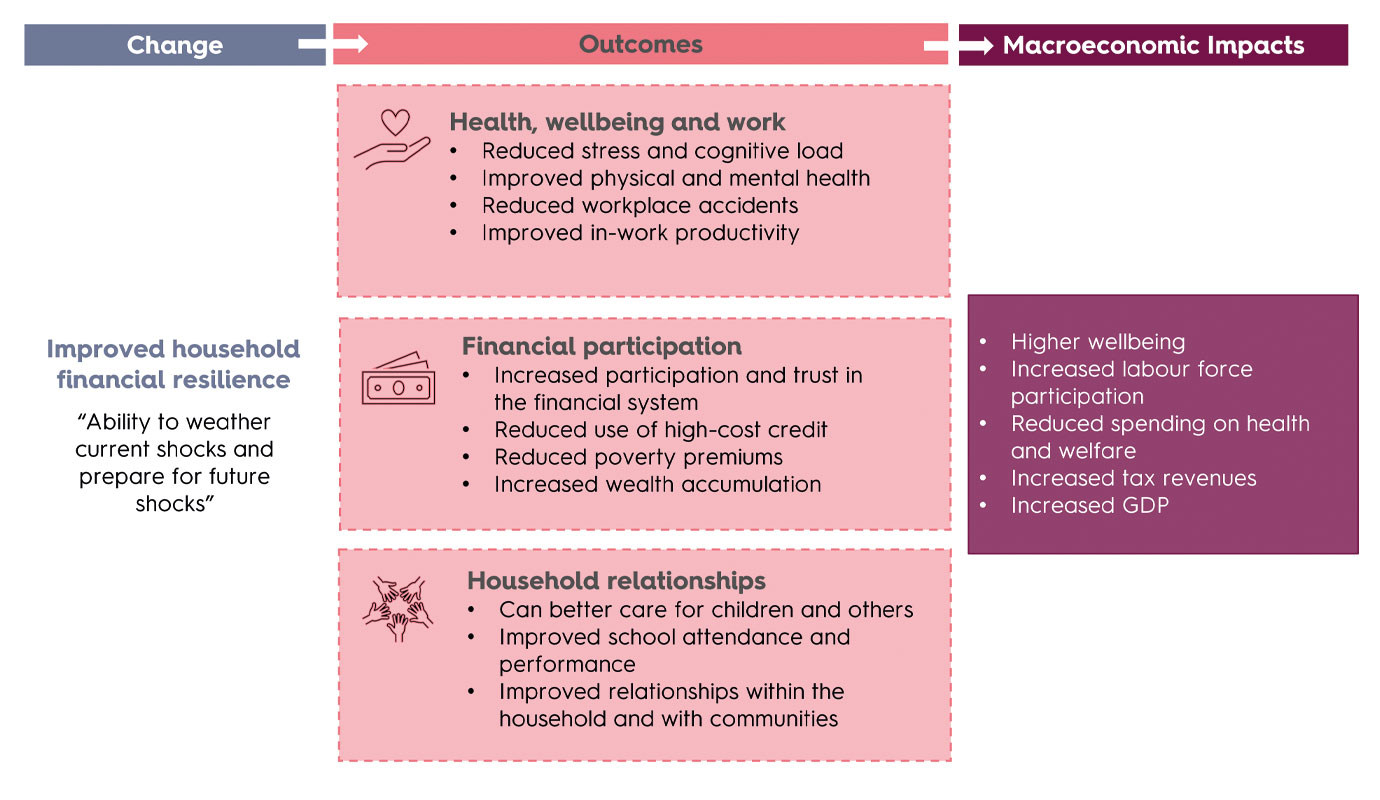

The financial resilience logic model

Building on this model, our work is focusing on three key areas:

Building on this model, our work is focusing on three key areas:

- Health, wellbeing and work: financial resilience can contribute to reduced stress and cognitive loads, leading to better physical and mental health, which in turn can help reduce workplace accidents and increase productivity.

- Financial participation: financial resilience can help reduce reliance on high-cost credit, reduce poverty premiums, and support wealth accumulation.

- Household relationships: within households with children, financial resilience might mean that individuals are in a better position to care for their children and contribute to a more supportive home environment. This may lead to improved school attendance and performance, which in turn is expected to have an impact on the employment and earnings prospects of these children when they reach adulthood.

Combined, these individual-level impacts could lead to increased labour force participation, reduced government spending on health and welfare, increased tax revenues, higher wellbeing and economic growth.

There is already an emerging evidence base on the importance of some of these effects. Saving is associated with better mental wellbeing, better sleep and higher life satisfaction.[3] Financial resilience has also been found to have a positive impact on our work and productivity. Research by academics in the US, using a two-year field trial with truck drivers, found that helping drivers build resilience through an emergency savings programme improved work performance – as measured by the number of traffic violations – for those with the highest levels of financial insecurity.[4] Separate research by the AARP’s Public Policy Institute found that individuals with emergency savings were more likely to report higher self-assessed job performance, a greater likelihood of receiving a pay rise or promotion, higher job satisfaction and lower turnover.[5] In terms of the impacts of financial resilience on individual finances, StepChange has estimated that having £1,000 in accessible savings reduces the risk of problem debt by almost a half.[6]

As part of this research programme, we are bringing together the existing evidence, and building up the evidence base where this is lacking, for example by analysing the extent to which improved financial resilience affects individual healthcare usage and labour force participation, or by unpicking the relationship between improved financial resilience and other financial behaviours.

At the aggregate level, we are not just interested in how financial resilience affects public finances and economic growth, we also want to understand the implications of financial resilience for the type of growth and for other important metrics such as subjective wellbeing. We want to highlight the myriad ways in which improved financial resilience affects the economy and society, with implications not only for the government’s growth agenda, but also public policy in areas including child poverty, mental health, and economic abuse.

We’re already seeing some interesting results. For example, our research shows that those with low financial resilience visit their GP more frequently: almost one in four people (23%) with very low financial resilience visited their GP three times or more in the previous year, compared with one in seven people (15%) with very high resilience.[7] People with low resilience also report being in poorer health than people with more resilience. In the coming months we’ll be sharing more of the findings across the themes described above as we seek to understand the scale of these potential benefits.

Vivien Burrows, Senior Research Economist at Nest Insight

To stay up to date with our latest research and events, sign up to our mailing list.

[1] FCA (2025). Financial Lives 2024 data tables (2. Attitudes, tables 37 and 39).

[2] Nest Insight (2026). Spotlight on… financial resilience

[3] PFRC (2024). Understanding the role of savings in promoting positive wellbeing

[4] C. Leana, X. Yang, D. Berkowitz & D. Kamran-Morley (2025). The effect of an emergency savings program on employee savings and work performance: a two-year field intervention. ILR Review, 78(5), pp. 806-831.

[5] M. Rao, J. Burke & D. John (2024). Does saving for emergencies improve productivity at work? AARP Public Policy Institute Research Report.

[6] StepChange (2014). Savings and problem debt

[7] Nest Insight (2026). Spotlight on… financial resilience